I’ve written here, here and here about how Monroe County likes to manipulate numbers. This post is about the document that was prepared in order to stifle talk of incorporation by creating the impression that Key Largo isn’t much of a contributor. The mythical small contribution also serves as an excuse to justify the wastewater funding inequity. There are a couple of obvious problems with this contention:

- It is factually incorrect. I’ve already discussed Key Largo’s contribution to the infrastructure sales tax here and here. Key Largo’s contribution to taxable property values is discussed here.

- It is irrelevant. When it comes to wastewater funding, the size of Cudjoe Regional’s contribution certainly doesn’t matter so why should Key Largo’s? I’ve compared the two here and here. I will mention it again throughout this post.

My primary mission here is to show how the county spins the numbers. It’s much more difficult for them to mislead an informed public. My secondary mission is to take an honest look at the numbers to see if Key Largo really would be better off incorporating. What I’ve seen so far strongly indicates that they would. Here is a link to the above-mentioned report prepared by the county. Let’s take a look at the general fund revenues.

Key Largo-Tavernier-impact (1)

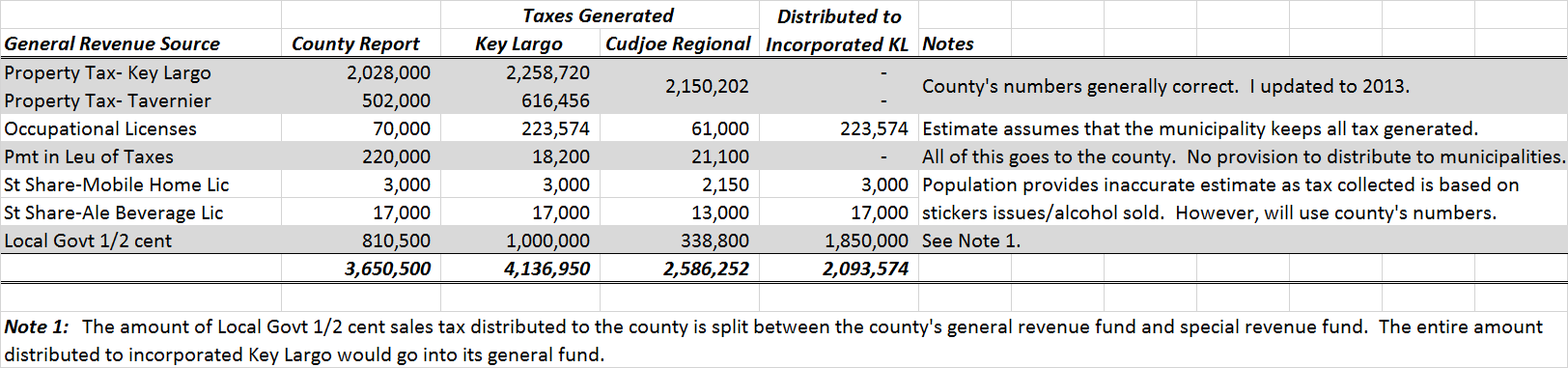

Property Tax contributed to the General Fund.

These numbers actually appear to be correct. However, it looks like they came from FY 2012. I’m going to use numbers from 2013. Even if Key Largo were to incorporate, it would still contribute this to the county’s general fund. Here is a link to the document for FY2013: ContributionTable_2013. In FY2013, Key Largo, including Tavernier, contributed about $2.8 million in ad valorem taxes to the general revenue fund. The Cudjoe Regional area contributed about $2.1 million.

Occupational Licenses (Business Tax).

It looks like whoever prepared the county’s report based the estimate off overall county-wide population (including incorporated areas). Clearly this would give an inaccurate estimate of how much is collected in each area. Obviously an area with little business activity isn’t going to generate much business tax. Unfortunately, the Tax Collector’s database provides no way to figure out the dollar amount collected in each area. However, there is information on the number of businesses in each area and the number of business tax units assigned to each business by the tax collector. The table I generated from that database is provided below.

The county collected $417,000 in the business tax in 2013. Assuming, the county collects only from the unincorporated area, Key Largo generated about 47% of that or about $223,600.

You’ll notice that this is actually quite similar to the proportion of sales tax generated. As the saying goes: Truth converges, bullshit diverges.

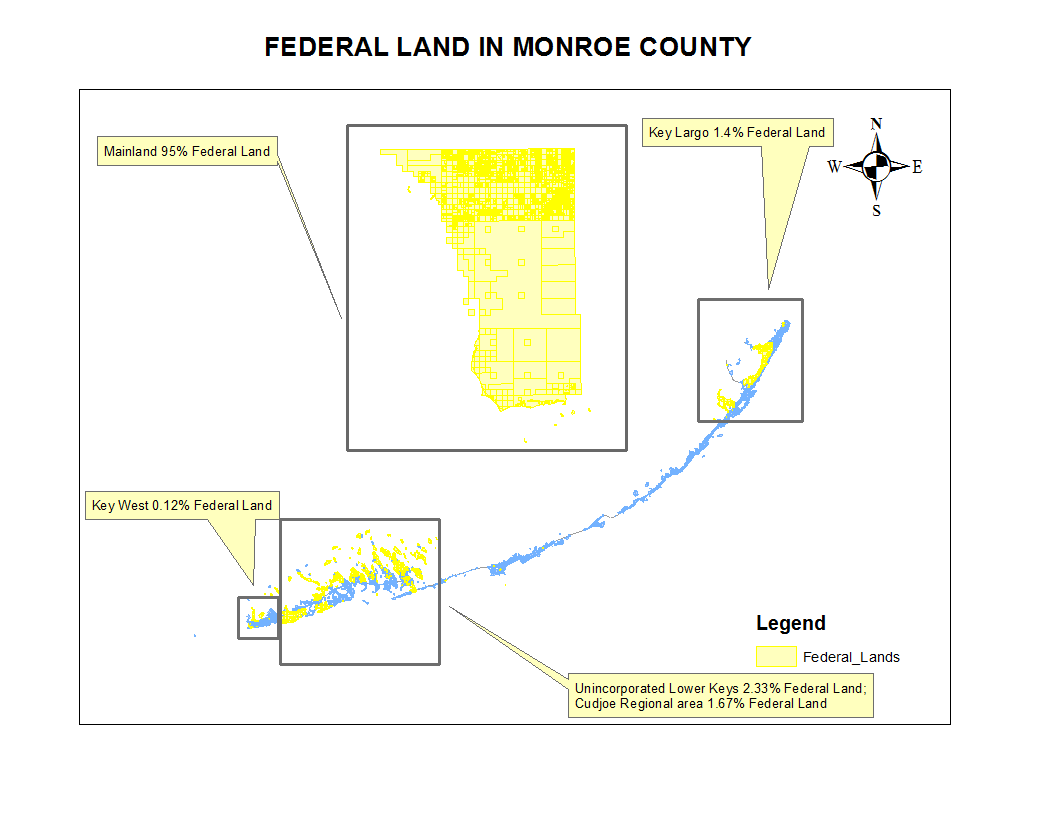

Federal Payments in Lieu of Taxes (PILT).

This is a payment received from the federal government. Land owned by the federal government is exempt from local property taxes. These payments help offset that exclusion. According to data I’ve got from the Monroe County Property Appraiser, 95%, of federally owned land is on the mainland. According to the Loger report, Monroe County received $1,243,189 from this source FY 2013. The truth is that very little of that was because of the islands. It’s almost entirely because of the mainland. If you look at the amount of federal land owned on the islands, Key Largo’s contribution is about 1.3% or $18,200. I estimate that Cudjoe Regional’s contribution is about 1.7% or about $21,100. Below is a map of federal lands within Monroe County. The truth is none of the islands, including Key Largo, generate very much of this.

State Revenue Sharing – Mobile Home Licenses and Alcoholic Beverage Licenses

Monroe County collected $93,656 and $223,250 from these two sources respectively in FY 2013. The small amounts won’t have much of an impact on the bottom line, so I won’t spend much time researching. For the purposes of this discussion, I’ll accept the county’s numbers on these two taxes.

From the Local Government Handbook here some information on the Mobile Home Licensing tax.

Summary:

Counties, municipalities, and school districts receive proceeds from an annual license tax levied on all mobile homes and park trailers, and on all travel trailers and fifth-wheel trailers exceeding 35 feet in body length. The license taxes, ranging from $20 to $80 depending on vehicle type and length, are collected in lieu of ad valorem taxes, and a sticker is issued as evidence of payment.1 Half of the net proceeds are remitted to the respective district school board. The other half is distributed to the respective municipalities depending on the location of such units or the county if the units are located in the unincorporated area. The use of the revenue is at the discretion of the governing body.

Also from the Local Government Handbook, here is some information on the Alcoholic Beverage tax:

Summary:

A portion of an annual state license tax levied on manufacturers, distributors, vendors, brokers, sales agents, and importers of alcoholic beverages and collected within a county or municipality is shared with those local governments. An annual license tax is imposed on the following: 1) any person operating a bottle club;1 2) vendors of malt beverages containing alcohol of 0.5 percent or more by volume, manufacturers engaged in the

business of brewing only malt beverages, or distributors of alcoholic beverages containing less than 17.259 percent alcohol by volume;2 3) vendors authorized to sell brewed beverages containing malt, wines, and fortified wines; authorized wine manufacturers; or distributors authorized to sell brewed beverages containing malt, wines, and fortified wines in counties where the sale of intoxicating liquors, wines, and beers is permitted;3 4) vendors permitted to sell any alcoholic beverages regardless of alcoholic content, persons associated together as a chartered or incorporated club, and any caterer at a horse or dog racetrack or jai alai fronton;4 and 5) authorized liquor manufacturers and distributors as well as brokers, sales agents, and importers, as defined in s. 561.14(4)-(5), F.S.5Distribution of Proceeds:

Twenty-four percent of the eligible taxes collected within each county is returned to that county’s tax collector.7 Thirty-eight percent of the eligible taxes collected within an incorporated municipality is returned to the appropriate municipal officer.8

As you can see an incorporated Key Largo would be entitled to a decent portion of both these revenue sources under state law.

Local Government Half-Cent Sales Tax

A total of $15,373,485 was distributed to Monroe County in FY2013. As we know, the Key Largo/Tavernier area generates about 15% of that county-wide or $2.3 million. About $4.0 million (44%) of that $15.4 million goes into the general fund, and roughly $5.1 million (56%) goes into a special revenue fund. The remaining $6.2 million is distributed to the municipalities. So of the $2.3 million generated by Key Largo, let’s say that 44% goes to the general fund or about $1 million; and about 56% or $1.3 million goes to special revenue. The Cudjoe Regional area contributes about 5% to the sales tax or about $770,000. Forty-four percent of that is $338,000 and 56% is $431,200.

An incorporated Key Largo would receive an estimated $1.85 million. Overall county revenues from this source would decrease by about $1.3 million if Key Largo were to incorporate. The municipalities would take a hit, too. Key West’s revenues would decrease by about $360,000. Of course, my concern here is Key Largo.

Wrap Up

I’ve thrown a lot of numbers at you. Now I’ll try to put them in some sort of context. See the table below.

The point of the county’s report was to understate Key Largo’s contribution. Cudjoe will receive about $60 million more in funding from the infrastructure sales tax than Key Largo will. Yet these numbers show that Key Largo contributes significantly more to the general fund than the Cudjoe Regional area does – about $1.6 million. Also significant, incorporated Key Largo would receive about $2.1 million to its general revenue fund.

Interestingly, the county excluded several revenue sources from its analysis. Most notably, state revenue sharing proceeds. About $3.8 million was distributed to the Keys in 2013; and $2.1 million of that went to Monroe County. The other $1.7 million was distributed to the municipalities. Also missing are local option taxes, which contributed nearly $4 million to the general revenue fund. I’ll take a look at these in subsequent posts.