I’m still digging into Monroe County’s “white paper”, which was written by Monroe County staff in support of Comm. Carruthers’s new sales tax, the Emergency Services Surtax (ESS). The “white paper” claims that by paying for fire and emergency services with this new sales tax instead of with property taxes the tax burden will shift from locals to tourists. This conclusion is based on some dubious “logic”.

I’m still digging into Monroe County’s “white paper”, which was written by Monroe County staff in support of Comm. Carruthers’s new sales tax, the Emergency Services Surtax (ESS). The “white paper” claims that by paying for fire and emergency services with this new sales tax instead of with property taxes the tax burden will shift from locals to tourists. This conclusion is based on some dubious “logic”.

- The “white paper” claims that locals pay 100% of the property taxes and tourists pay 0%. I think most people would laugh out loud at that one. I ran the numbers here. According to my estimate, locals actually pay about 47% of the property taxes and that’s without taking the Homestead Exemption into account. Locals actually pay a bit less than 47%.

- The “white paper” also claims that that locals will only contribute an additional $125 per year to this new sales tax. This claim is not mathematically possible using the county’s own numbers. Nor can it be corroborated using other data sources. The number looks to be in the $400-$500 range.

- The “white paper” obscures the impact on locals by “flattening” the data and focusing on one favorable scenario – a $350,000 single family home. In fact, Key West locals will typically pay more for fire and emergency service because of this new sales tax. Homeowners will contribute about $130 more per year.

- Making matters worse, Key West has a very high proportion of renters. Those folks, of course, will contribute the full $400 to the new sales tax. There won’t be any offset from the property tax reduction for them.

- The real beneficiaries actually seem to be wealthy property owners, many of whom live outside Monroe County.

As it turns out, the “white paper” is also deceptive about the impact of the “tax shift” on the City of Marathon. It claims that property taxes for Marathon homeowners would be reduced by 70%. Wow! That’s an attention-grabbing number.

In this post, I attempted to reconcile my numbers with the county’s. We’re pretty close when it comes to Monroe County, Key Largo and Key West. On Marathon and Islamorada, we are miles apart. So let’s take a close look at how Monroe County staff arrived at their number for Marathon.

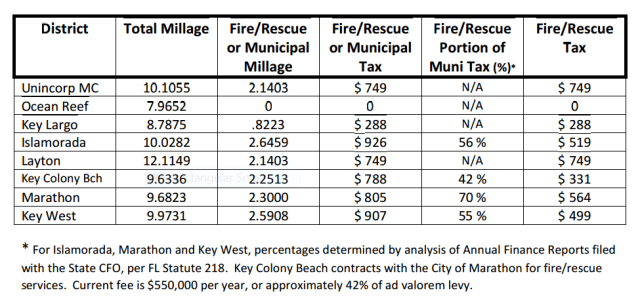

Here’s their table again. And here’s a link to the agenda back-up containing the “white paper”.

Here is an excerpt from the “white paper” explaining what assumptions were used.

The tables below summarize the 2014 financial impact on property owners in each of the 8 taxing districts within Monroe County. The following assumptions were used.

• Assessed value of $350,000

• One percent sales tax generates $34 million countywide

• Countywide fire/rescue spending equals $29 million

• Ambulance revenues of $3 million are offset against fire/rescue spending

I’ll be honest, I have no idea where the county got their numbers for Marathon. The closest I can come is to take the amount of spent on fire and ambulance service according to the 2014 CAFR (page 55) and divide it by the total amount of ad valorem taxes collected. That is $2.7 million divided by $3.95 million – or a little over 68%.

The county’s math works okay when you’re talking about very straightforward situations. Monroe County and Key Largo have an ad valorem tax specifically for fire and ambulance service. It looks like Key West only pays for fire and emergency services with ad valorem taxes. The only exceptions might be capital purchases made with infrastructure sales tax money.

Marathon’s situation is a bit more complicated. For one thing they serve the city of Key Colony Beach (KCB). The county included Key Colony Beach in its analysis as a separate entity, which is fine. But if they’re going to do that they need to exclude the cost of serving Key Colony Beach from Marathon’s cost.

If they don’t, they’re double counting it and over-stating the reduction to ad valorem taxes. They did something similar with their wastewater funding analysis. Either the county loves lying with numbers or they’re just really bad at math.

I took a different approach. I took the average amount spent on fire and rescue services by each entity over the past few years, converted that to a millage rate and applied it to the taxable value for each entity. This to me, seems more in line with the intent of the law. Either way, it’s done I should be able to reconcile my number with the county’s. We won’t be exactly the same, but we should come pretty close.

The City of Marathon does not appear to break out the cost of fire and ambulance service to Key Colony Beach in it’s financial documents. So to avoid double counting Key Colony Beach’s contribution, I combined them with Marathon.

To correct the county’s math, I disregarded Key Colony Beach’s annual payment of $550,000. The logic being that the cost to serve KCB is already included in the $2.7 million. If I do that, we get a number that makes a bit more sense than 70%.

$2.7 million – $550,000 = $2.15 million

$2.15 million/$3.95 million = 54%

54% * 2.3000 = 1.2420

And that is a lot closer to my number for Marathon, which was 1.1568.

Alternatively, I could take the combined cost of fire service divided by the combined ad valorem tax collections for Marathon and Key Colony Beach.

$2.7 million/($3.95 million + $1.22 million) = 52%

Either way yields a similar result.

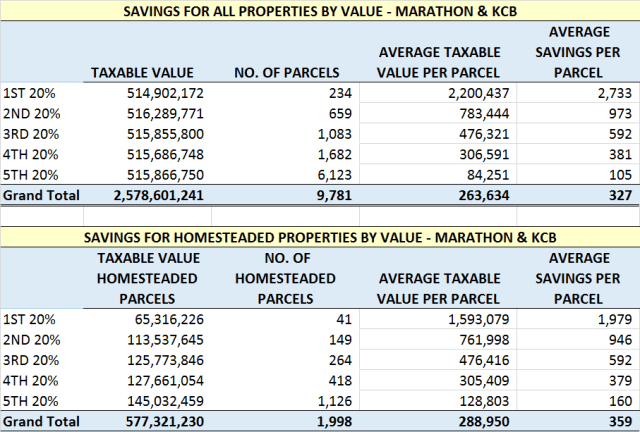

Here is my table, revised to take that change into account.

So what does Carruther’s “tax shift” really mean for Key Colony Beach and Marathon?

This is the same table, I used in the Key West post except that I revised Monroe County’s millage rate for Marathon to correct for the contribution from Key Colony Beach, which appeared to have been double counted in the county’s original calculation.

It looks like local homeowners in Marathon and KCB will contribute between $58 and $83 more per year, depending on whose numbers are used. No savings for them.

As in Key West, most of the homesteaded properties are clustered in the lowest 20% by value. The average taxable value of those homesteaded properties is about $129,000. That yields a savings of $160 for the typical local homeowner in Marathon and KCB. However, Carruther’s scheme will also require those homeowners to pay $417 more in sales tax. So instead of saving money, these folks will pay about $257 more per year.

Poor Comm. Neugent thinks he’s going to break even. That does not appear to be the case at all. Better break the bad news.

Of course, local residents who rent instead of own will be even more heavily impacted as their is no property tax reduction to offset the additional sales tax.

Monkey math strikes again!

Conclusions and caveats: This ESS nonsense is still in the preliminary stages. There isn’t enough information yet to determine what the impact on locals will actually be. However, it is clear at this stage that Monroe County’s numbers are not accurate. It is hard for me to see this “white paper” as a good-faith effort to quantify that impact. Fact-checking continues.