Update: Not sure which Dan/Danny/Daniel Kolhage is involved in the businesses discussed in the last paragraph. There’s more than one apparently. In any case, there are still some unexplained holes in county commissioner Danny Kolhage’s financial disclosure forms. Undisclosed involvement in side businesses might have explained some of that. This is an important issue.

Kolhage claims to be a supporter of financial restraint. Despite the occasional grandstanding, Kolhage is one of the leading proponents of reckless spending on the Board of County Commissioners (BOCC). His voting record makes that abundantly clear. Spending and debt has sky-rocketed on Kolhage’s watch, with his full and enthusiastic support. Voters pay more attention to Kolhage’s empty words than they do his actions. Unfortunately, they are paying through the nose for that mistake. Kolhage may simply be foolish with taxpayer money or it could be something far more troubling. I think we owe it to ourselves to find out.

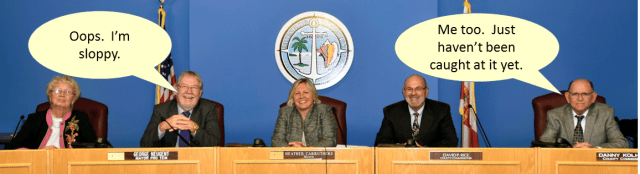

This topic has been simmering for a while. I finally decided to publish a post about it because Commissioner George Neugent is facing sanctions from the Florida Ethics Commission (FEC) over incomplete financial disclosures, and the failure to report a free country club membership. I’m just amazed that any county official would face consequences for anything ever. The Board of County Commissioners (BOCC) typically operates a laissez-faire operation, completely lacking in accountability. I guess Neugent, at least, made the mistake of thinking everyone else thinks that’s okay.

The BOCC allowed the county administrator, Roman Gastesi (known around here as the iPhone Bandit), to get away with purchasing iPhones stolen from the county. He purchased them for cash at deep discounts. He had to know something was up. Comm. Heather Carruthers scored a hot iPhone for herself so I guess she wasn’t about to nail anybody else for it. A 2014 audit showed that Rice, Neugent, Carruthers, and Gastesi had misused their county purchasing cards. Rather than simply apologizing and making it right, Carruthers wrote a high-handed, excuse-ridden response to being called out on it.

On top of that, there’s the sleazy and incompetent way the commissioners conduct the people’s business. Consistently going over budget on capital projects. Failing to properly oversee the wastewater projects. Distributing funding in a negligently unfair way. Lies, lies and more lies – which they double down on when they’ve been caught.

Neugent called his infractions “sloppy paperwork”. I find that incredibly ironic. You see the ethics complaint filed against Neugent grew out of the Stand Up for Animals (SUFA) debacle – a county-initiated witch hunt. In his deposition, Gastesi (of all people!) accused SUFA of “sloppy bookkeeping“. (See page 7.) In the end, the county agreed to pay SUFA $45,000. I guess SUFA wasn’t the sloppy one after all.

Elected officials, appointed officials and certain public employees are required to complete and submit financial disclosure forms. Fortunately for us, this includes our county commissioners. In fact, their financial disclosure forms for the past four years are available online at the Florida Commission on Ethics. You can do your own search here.

I reviewed the forms for each one of the five. Neugent’s “sloppiness” not withstanding, one really stood out from the rest. That would be Comm. Kolhage. Here are links to each of the four reports available online: 2012, 2013, 2014, 2015. The numbers Kolhage reported raise a few questions in my mind.

- For each year, there are large differences between reported net worth and calculated net worth. The reported net worth should include assets and liabilities under $1,000 or less. These don’t have to be specifically listed on the form. To come up with calculated net worth I deducted reported liabilities from reported assets. Reported net worth is what is shown at the top of the page. The difference ranges from $100,000 to $271,000, which would mean either Kolhage has a hundred or so items under $1,000 or he’s not reporting everything.

- There are some very large jumps in asset values. From 2012 to 2013, total asset value jumped by $343,000. From 2013 to 2014, asset value jumped by another $137,000. Some of that could be explained by depositing income into cash or investments. Some of it could be explained by appreciation. Still, these are huge unexplained jumps in a short period of time.

- These seeming discrepancies prompted me to check out Mr. Kolhage’s business ties on SunBiz.com. I was already aware that he’s been an officer in numerous short-lived business ventures. I wrote about one here and another here. He doesn’t list any secondary income on his financial disclosure forms. Is it possible that there is unreported income from these businesses? Is that why his cash and investments increased so much in some years?

Is Kolhage reporting all the information required? The holes in his financial disclosure forms indicate that he may not be. Sloppy, like his audit of SUFA.

Here’s a table I put together of Kolhage’s financial disclosure forms from the last four years. Filers are required to list secondary sources of income. That is income over $1,000 from businesses in which the filer holds an interest. Kolhage was an officer in at least three businesses over the reporting period covered. The businesses that were active over that time period are listed below. Note that the last one was incorporated in 2016 so it wouldn’t have generated any income in 2015.

- Kolhage’s, Inc.: 5/15/2015 to present.

- Appalachian Appliance Company: 5/28/2013 to 9/26/2014.

- M&M Construction Company of Key West: 7/19/2004 to present.

- All Keys Property Service, Inc.: 6/27/2016 to present.

Interesting stuff. Don’t know if an ethics complaint would go anywhere, but maybe it’s worth looking into.